The American dragon shows its teeth

How Geopolitics Pressures the Current Market

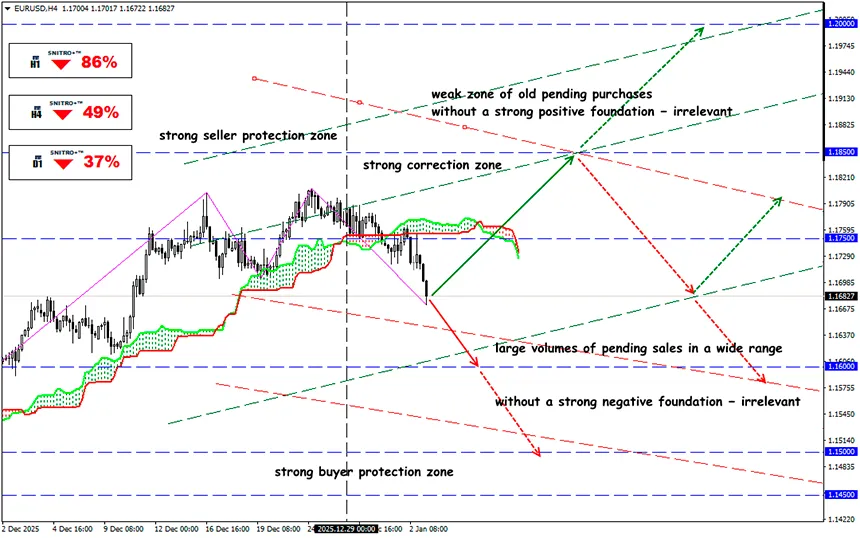

EUR/USD

Key zone: 1.1650 - 1.1750

Buy: 1.1750 (on strong positive fundamentals) ; target 1.1900; StopLoss 1.1680

Sell: 1.1620 (on a pullback after retesting the 1.1700 level) ; target 1.1500; StopLoss 1.1680

The return of Trump to the active political agenda was initially perceived by markets as a factor of increased volatility. An era of tough and unconventional decisions is predictably accompanied by strikes against the global political architecture; however, traditional market mechanisms for adapting to such pressure have proven ineffective.

At the current moment, from the stated objectives Trump has achieved:

- A weaker dollar, rising equity markets, and low oil prices;

- Activation of the process of forming new trade agreements, while problems in relations with China persist;

- The digital dollar project has effectively been shut down: the Federal Reserve is legally prohibited from issuing a CBDC, and cooperation with the BIS has been terminated;

- Tax reform has been implemented in the format of extending the first-term tax cuts and has been approved by Congress;

- The use of private stablecoins backed by U.S. Treasury bonds has been authorized.

Among the unfulfilled objectives, Trump still has the reduction of the Fed’s key rate, the yield on 10-year Treasuries down to 1%, as well as cheaper mortgage lending. In addition, Trump stated that he wants to acquire Greenland, make Canada the 51st state, and obtain full control over the Mexican (now — American) Gulf, but the events of last week showed that American ambitions are far broader.

The justification of a possible military operation in Venezuela became an indicator of how Trump’s team plans to advance its goals, and under these conditions markets will have to search for defensive strategies.

Trump publicly confirmed the return of the United States to the Monroe Doctrine, which in practice means the restoration of American dominance in the Western Hemisphere. Such a course implies a new configuration of global agreements, under which Europe loses U.S. political and military protection, while China, at a minimum, regains control over Taiwan.

The question remains open whether a potential attack on Venezuela was coordinated with Beijing and how the Taiwan scenario will develop. A military option would lead to a sharp collapse of the U.S. stock market, since the American economy still critically depends on Taiwanese production of advanced AI chips — TSMC’s capacity cannot yet be quickly replaced domestically.

Against this backdrop, European assets, Taiwan, and shares of companies dependent on Taiwanese supplies remain leaders of the equity market. A potential cancellation of Trump’s April visit to China may become a trigger for a large-scale geopolitical crisis.

Key market theses of the current stage:

- The loss of the Fed’s independence remains one of the key market fears. At the same time, rate cuts do not imply an automatic increase in demand for Treasury Bills: if inflation accelerates, investors may, on the contrary, exit U.S. T-Bills;

- Tariff policy has lost its destabilizing role. A Supreme Court decision on tariffs may cause a short-term correction but will not change the strategic picture. Even in the case of a negative verdict, Trump will offset one decree with dozens of new ones, and there will be no refund of tariffs to taxpayers;

- The risk of a new U.S. shutdown remains from February 1 if no compromise is reached on healthcare insurance. Market reaction and consequences are expected to be similar to the autumn crisis.

- In the medium term, it is important to monitor the Japanese yen: a mass exit from carry trade may trigger a significant liquidity outflow, primarily from U.S. assets. Against the backdrop of expected Fed rate cuts and gradual tightening by the BOJ, the U.S.–Japan yield spread is narrowing, which traditionally weakens the dollar against JPY.

- The ECB keeps rates unchanged with the possibility of later adjustments. A less restrictive monetary policy supports the euro, while policy divergence (Fed — downward, ECB — stability or potential tightening) forms a foundation for strengthening EUR/USD.

Pressure on the dollar persists amid diverging monetary policies. Escalation of economic and political pressure from the Trump administration increases the dollar risk premium, reinforcing bearish sentiment on USD against EUR, GBP, and AUD, especially during periods of conflict escalation. Under such conditions, deep fundamental analysis ceases to be an option and becomes a mandatory element of any trading strategy.

So we act wisely and avoid unnecessary risks.

Profits to y’all!