The ghost of a truce in the commodity market

What will happen to oil prices

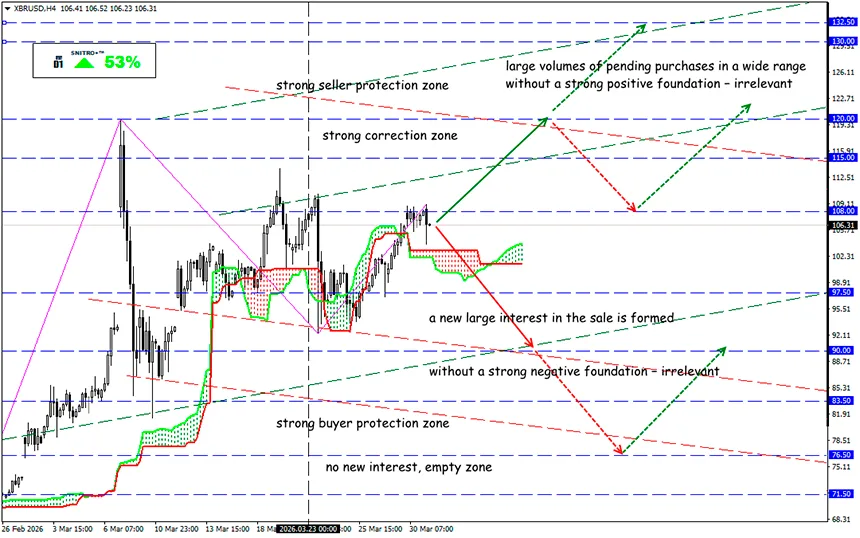

XBR/USD

Key zone: 105.00 - 108.00

Buy: 108.50 (on strong positive fundamentals); target 110.50-112.00; StopLoss 107.50

Sell: 103.50 (on a decisive break above 105.00); target 100.00; StopLoss 104.50

In March, the price of Brent crude rose by more than 55% — one of the strongest monthly jumps in history. The market is now preparing for a new test of the $100–108 zone after the Yemeni Houthis effectively opened a new front in the conflict with Iran. Supply logistics in the region remain seriously disrupted.

Brent futures for May delivery gained about 2.5% (above $115), while WTI futures rose by roughly 1.5% (above $101). Additional tension in the market was caused by statements from Trump about a possible “seizure of oil” in Iran and redirecting it to other markets.

Let us recall:

fields is now flowing directly to the U.S. market.

In recent years, any sharp rise in oil prices has been driven not so much by demand as by supply risks. At the moment, the key threats are concentrated around transport routes:

- The Strait of Hormuz remains the main bottleneck of the global oil market;

- alternative routes, including the Bab el-Mandeb Strait between the Red Sea and the Gulf of Aden, cannot fully compensate for potential losses;

- about 4–6 million barrels of oil pass through Bab el-Mandeb every day, and it is technically impossible to increase this volume quickly.

By the way, Saudi Arabia has increased oil exports through the Red Sea to nearly 5 million barrels per day, which allows it to compensate for about 45% of the volumes that previously passed through the Strait of Hormuz.

- Stock markets are increasingly pricing in not just a short-term spike but a more prolonged rise in the cost of Brent crude and possible interest rate increases. A prolonged blockade of the Strait of Hormuz could increase the risk of recession — not only in the United States, but also in countries in the conflict region.

- One of the most dangerous scenarios is considered to be a possible strike on Iran’s main export hub — Kharg Island, through which about 90% of the country’s oil exports pass. In that case, the market could face a large-scale supply deficit and a new round of escalation across the entire Persian Gulf region.

- Even if alternative routes through the Suez Canal are used, their capacity is not sufficient to fully compensate for possible disruptions. Supply losses could reach 4–5 million barrels per day.

So what is the result?

At the moment, the oil market is effectively operating in a force-majeure mode — and this situation has been continuing for several weeks. Even if signals of possible de-escalation appear, restoring normal shipping through the Strait of Hormuz may take time and may not happen before mid-April.

At the same time, a stable long-term rise in oil prices looks unlikely: prices that are too high inevitably create the risk of a global recession. If we look at a horizon of more than six months, a gradual decline in prices may become the more likely scenario.

There is also a fundamental factor: once prices reach $150 and above, consumers begin to sharply reduce demand, companies start saving energy, and the development of alternative energy sources accelerates. As a result, the market may stabilize within a broader range — roughly $120–150.

Investors are now actively looking for a “pain point” that could force Trump to change his approach to the conflict. The consolidated forecast of many analysts still remains around $125 per barrel for Brent crude.

The main conclusion: short-term volatility may remain extreme, but in the long term it is the risk of recession — not geopolitics — that is most likely to become the key factor for the oil market.

So we act wisely and avoid unnecessary risks.

Profits to y’all!