Oil: between fear and reality

How the current crisis differs from classic scenarios

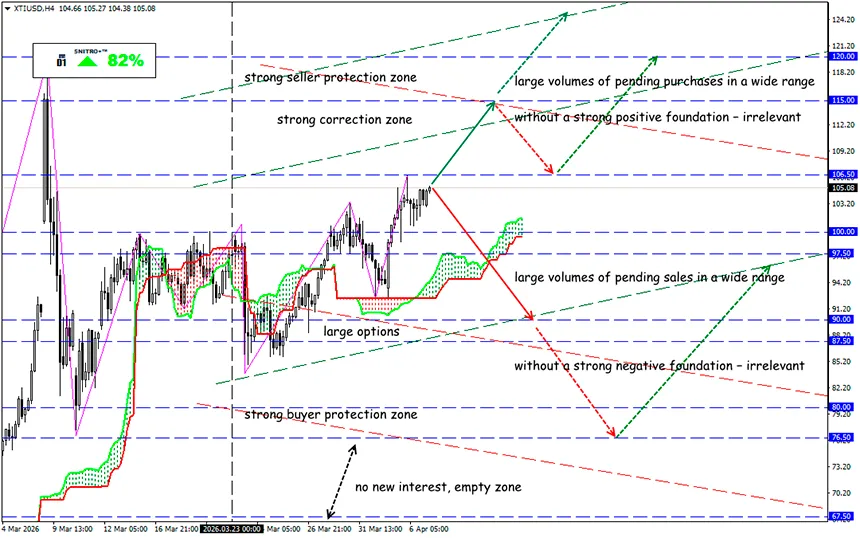

XTI/USD

Key zone: 102.00 - 107.00

Buy: 107.50 (after retesting the 105.00 level); target 112.50-115.00; StopLoss 106.50

Sell: 100.00 (on strong negative fundamentals); target 95.50-90.00; StopLoss 100.70

The oil market is living in a state of constant tension: statements by Donald Trump continue to push prices higher amid the conflict in the Middle East. At the same time, paradoxically, the actual blockade of supplies through the Strait of Hormuz is gradually fading into the background. The overall level of military escalation is becoming far more important.

Europe and the Persian Gulf countries are effectively running out of political tools to contain the economic consequences. And this is exactly what makes the current crisis unique.

Why this crisis is different from previous ones

The oil shock has exposed a new vulnerability: for the first time, the global economy is facing a crisis of this scale against the backdrop of an already overloaded financial system.

Reminder:

During the oil crisis of the 1970s:

- budget deficits of key countries were around 2% of GDP;

- public debt levels were relatively low.

Today the situation is radically different:

- the average budget deficit has more than doubled;

- government debt of G7 countries exceeds 100% of GDP;

- global debt has reached $348 trillion — more than three times global GDP.

This means governments have almost no room left for stimulus measures.

Old methods no longer work

Governments are trying to act according to familiar patterns: introducing price controls, using rationing mechanisms, subsidizing fuel. But bond markets are already signaling risks: rising spending could lead to a debt crisis.

Central banks are also trapped: the oil shock slows the economy but at the same time increases inflation. In such a situation, cutting rates is dangerous, and raising them is risky.

Who is most vulnerable

Countries with high debt and deficits are under the greatest pressure: the United States, the United Kingdom, Brazil, Egypt, Indonesia.

Only a few economies appear relatively resilient: Taiwan, Vietnam, Sweden. For example, Sweden’s budget deficit remains below 2% of GDP, providing more room for maneuver.

Even the United States, despite energy independence, is vulnerable: a budget deficit of about 6% of GDP is among the highest in developed economies.

What is happening in the oil market right now

The OPEC+ alliance has already warned: infrastructure destruction will lead to a prolonged recovery of supplies.

At the same time:

- an increase in production of about 206 thousand barrels per day is rather symbolic;

- actual supplies are constrained by war and logistical disruptions.

There are isolated attempts at stabilization:

- Iraq has announced a possible resumption of exports via the Strait of Hormuz;

- the tanker Ocean Thunder has already passed through the strait with a cargo of about 1 million barrels;

- Saudi Arabia has raised prices for Arab Light crude for Asia to record levels.

The market is driven by expectations, not facts

Prices are rising again after new ultimatums from Trump directed at Iran. But the key point is that the market is currently reacting not to an actual shortage, but to risks.

This creates unstable dynamics:

- any statement can sharply change prices;

- strikes on infrastructure are instantly priced in;

- reported data cannot be relied upon, statistics are moving to the background.

And what is the result?

If the situation does not stabilize:

- the $150 per barrel level could be reached very quickly;

- in the case of a severe deficit, market balance may only be possible above $200.

The main feature of the current crisis is not just rising prices, but the absence of tools to contain them. This is what makes the situation fundamentally more dangerous than in previous decades.

However, not all market participants believe in such a scenario. The so-called “smart money” is placing bets against extreme growth.

So we act wisely and avoid unnecessary risks.

Profits to y’all!