What to Expect from the “Black Gold” Market

Why Oil Is a Winner, Not a Victim

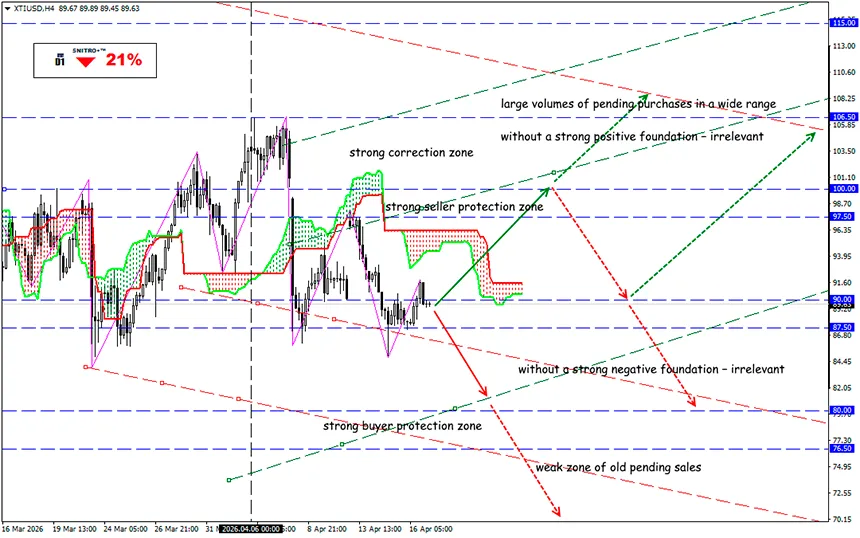

XTI/USD

Key zone: 87.50 - 91.50

Buy: 93.50 (on a strong positive foundation); target 97.50-100.00; StopLoss 92.50

Sell: 86.00(after retesting the 90.00 level); target 83.50-81.50; StopLoss 87.00

As of mid-April 2026, the oil market is not just trading with a geopolitical premium — it is operating in a dual-market regime: the physical market is in deficit, while exchange-traded futures are already pricing in partial de-escalation.

This is reflected in the sharp divergence between physical Dated Brent and Brent futures. According to WSJ estimates, on April 14, physical Dated Brent rose to around $132.7, while June Brent futures were near $99.4. At the same time, by April 17, futures prices had already pulled back to ~$96–98 for Brent and ~$88–93 for WTI on hopes of positive developments in negotiations.

For hedging, this is critical: the risk of demand spikes is currently much higher than usual. On the demand side, Asian importers are key, as about 80% of oil flows through the Strait of Hormuz in 2025 were directed to Asia, along with 84% of LNG. China and India together accounted for 44% of oil passing through Hormuz, while Japan and South Korea remained heavily dependent on these flows.

From a physical balance perspective, the conflict has already triggered one of the largest supply shocks in decades.

- According to the IEA, restoring energy production volumes in the Middle East could take around two years, depending on the country. In Iraq, the process will take significantly longer than in Saudi Arabia.

- The IEA estimated supply disruptions at nearly 4.7 million barrels per day (mb/d) in March, rising to about 9.1 mb/d in April, while regional refineries and some Asian processors reduced throughput by roughly 6 mb/d.

- The IEA also raised its average Brent price forecast for 2026 to $95.7 and for Q2 to $115, directly linking this to the loss of Iranian and neighboring supplies, as well as damage to Qatar’s LNG capacity.

The key risk node remains unchanged: the Strait of Hormuz. In 2025, nearly 20 mb/d of oil and petroleum products passed through it — about 25% of global seaborne oil trade. Alternative pipeline capacity outside the strait is estimated at only 3.5–5.5 mb/d.

Even with a formal easing of hostilities, any renewed blockade, inspections, port strikes, or pipeline disruptions can quickly translate into a physical shortage.

Over the next three months, the base-case scenario is not normalization but a managed deficit: supply partially recovers, but logistics, insurance, secondary sanctions, and maritime security remain binding constraints.

In this scenario, the most likely range for front-month Brent is $95–115, and for WTI $86–103.

A stress scenario, where an additional 10–20% of typical export flows tied to Hormuz are disrupted, implies $120–150 for Brent and $108–138 for WTI.

An extreme scenario, where disruptions exceed 20% of flows and alternative routes and/or the Red Sea/Bab el-Mandeb are also affected, implies $150–190+ for Brent and $135–175 for WTI.

In this context, strategies may include selling Brent versus WTI, maintaining long volatility positions, and selective long positions in distillates. And remember — the “Trump factor” is not fading; it is intensifying. Political rhetoric alone can trigger double-digit percentage corrections within just 2–3 trading sessions.

So we act wisely and avoid unnecessary risks.

Profits to y’all!