How the Big Tech Monster Is Saving the Global Market

Nvidia’s Report Beat Expectations

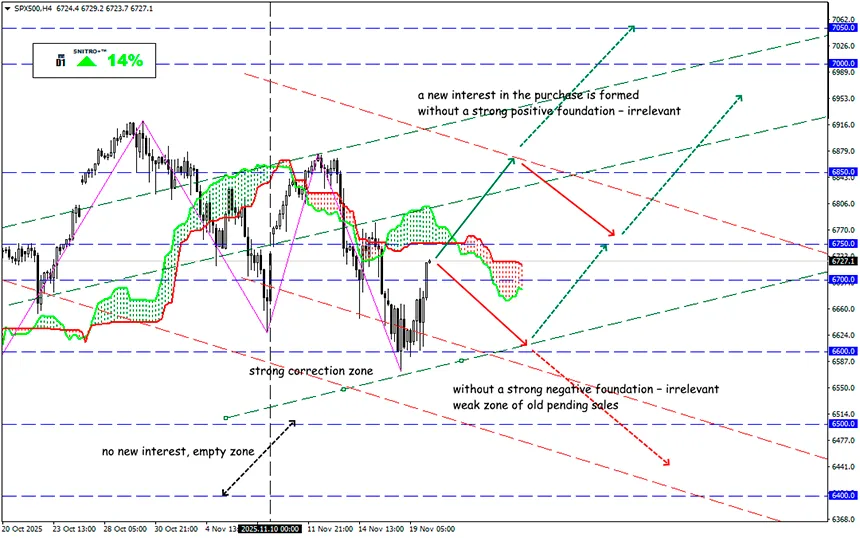

SP500

Key zone: 6,650 - 6,750

Buy: 6,800 (on a confident breakout of the 6,750 level); target 6,900-6,950; StopLoss 6,720

Sell: 6,650(on strong negative fundamentals); target 6,500; StopLoss 6,720

Nvidia didn’t even need a buyback to create an ultra-positive market backdrop. The main reaction, as usual, will appear after the U.S. exchanges open. However, it’s important to remember that this report does not create actual capital inflows into the market, including the crypto segment: NVDA’s financial metrics are formed through multiple turnovers of the same capital.

Reminder: Nvidia effectively finances OpenAI and several other companies (including deals with Anthropic) so they can purchase its high-performance chips. Thus, Nvidia increases future profits using its own funds — a model the company applies regularly and very effectively.

Main results:

- Revenue — around $57 billion versus expectations of ~ $54.9 billion (+62% y/y).

- EPS — $1.30 versus the forecast of $1.25.

- Data Center/AI segment recorded revenue of ~$51.2 billion, above expectations.

- Q4 guidance — over $65 billion in revenue (market expected 61–62 bn).

- NVDA shares gain about 6% in post-market.

Positive aspects of the report:

- Revenue and EPS beat forecasts, confirming stable demand for AI infrastructure.

- Strong Data Center growth indicates active corporate investment — a key indicator of trend sustainability.

- The company’s guidance exceeds market expectations — management shows confidence not in a temporary spike but in continued growth.

- Amid discussions of a potential “AI bubble,” Nvidia’s data temporarily reduces systemic anxiety: demand, contracts, and new architectures are functioning effectively.

Risks that cannot be ignored:

- Despite +62% revenue growth, the current share price already reflects excessively high levels of future profit. Yes, the results are strong, but the market may still be dissatisfied if doubts arise about the trend’s continuation.

- Management pointed to potential obstacles: energy constraints, export barriers (especially China), and the scale of rising infrastructure costs.

- Any slowdown in coming quarters could sharply expose overvaluation risks (P/E, P/S), increasing the probability of correction.

- Competition — AMD, Intel, new AI solutions — plus market saturation with infrastructure and rising operating costs create pressure on further growth.

What this means for a trader:

Positioning:

the report confirms the continuation of the trend in AI-infrastructure development. But buying without strict protection is unjustified — volatility will be high.

Hedging:

after a strong report, a technical pullback usually follows. Stop-Loss and options are mandatory.

Horizon:

- short-term strategies (H1–W1) may trade the initial market reaction;

- medium-term strategies should focus on industry trends, not single-quarter data.

Nvidia’s report is genuinely strong: revenue and profits exceeded expectations, and the forecast is optimistic. Since NVDA is a “barometer” of AI-infrastructure, its positive results reduce systemic risks for the sector, while any weak signals, on the contrary, amplify them. Traders should monitor the reaction of competitors and companies in adjacent segments.

So we act wisely and avoid unnecessary risks.

Profits to y’all!